Discover the captivating world of budgeting within the realm of fund accounting in our latest article. Delve into the intricate principles that guide transparency and accountability, unraveling how funds are meticulously tracked based on unique requirements and constraints. Unveil the art of setting financial goals, the orchestration of negotiations, and the meticulous dance of implementation, all while maintaining a delicate balance between fiscal responsibility and community needs. Explore how budgeting forms the backbone of fund accounting, a distinct universe where each fund tells its own story, fostering stewardship, and enabling impactful change. Join us on this enlightening journey where budgets aren't just numbers, but blueprints for a better future.

Budgeting

Fund accounting is an accounting system that is used by government agencies, non-profit organizations, and other entities that receive and manage funds from various sources. The purpose of fund accounting is to track financial resources based on their requirements and restrictions.

Fund accounting uses seven principles to uphold high standards of transparency and accountability. The first two principles focus mainly on where funds are being placed. Principle #1, the segregation of funds, guarantees that funds are used for their intended purposes, while the second principle, tracking restricted vs. unrestricted funds, ensures that restricted funds are not used for unintended purposes. The system of accrual accounting is the third principle of fund accounting, and it focuses on financial statements to accurately reflect a government’s financial health.

The fourth of these principles is budgeting. Budgeting is a critical part of fund accounting because governments and organizations must prepare and adhere to budgets that align with their goals and objectives. This principle ensures that resources are properly allocated and used in the most effective manner.

The first three principles of fund accounting rely heavily on the budgeting process. Fund segregation involves government agencies treating each fund as a separate accounting entity with its own set of accounts. Budgeting ensures that the inflows and outflows for each fund are allocated appropriately and that the funds are used in accordance with their designated purposes. While restricted funds cannot be used for anything except their designated purposes, budgeting aids in tracking unrestricted funds so that other needs within the agency or community are being met the most efficiently. Lastly, accrual accounting reflects a government’s financial standing by factoring in the revenues earned and expenses incurred during a specific period, regardless of the cash inflows and outflows. Without a proper budget in place, governments would not be able to identify variances and take corrective actions if necessary.

Budgeting first starts with setting financial goals for each fund. These goals could include expected revenues, expenses, and other financial targets. Local governments budget in a structured and comprehensive manner to manage their finances effectively and provide essential services to their communities, like infrastructure projects and community programs. The budgeting process begins with gathering financial data, revenue projections, and expense estimates from various departments and agencies within the local government. Each department or agency outlines its funding requirements based on the services it provides.

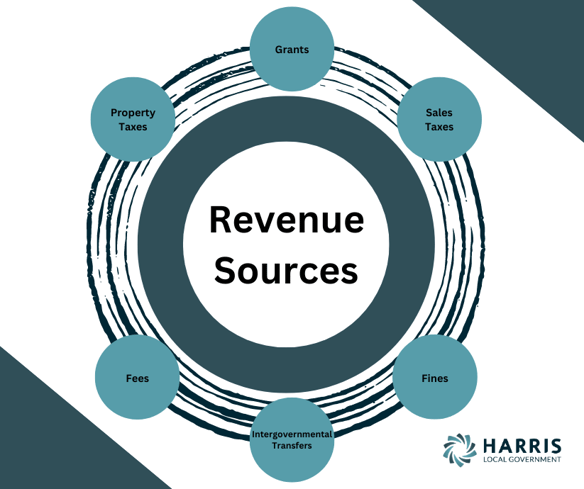

Local governments must estimate their revenues for the upcoming fiscal year. Revenues may come from various sources, such as property taxes, sales taxes, grants, fees, fines, and intergovernmental transfers. Accurate revenue projections are essential for creating a realistic budget. Many local governments also seek input from the public during the budgeting process. They may hold public hearings, town hall meetings, or solicit feedback through surveys to understand the community's preferences and priorities. Public input helps in shaping the final budget. Based on revenue projections and needs assessments, the finance department or budget office prepares a preliminary budget proposal.

The next step in the budgeting process is negotiations. The budget proposal may undergo adjustments based on feedback from department heads, elected officials, and the public. There might be reallocations of funds or revisions to reflect changing circumstances or priorities. Once the budget proposal is finalized, it is presented to the governing body, such as the city council or board of supervisors, for approval. Elected officials review and vote on the budget before it becomes official.

After approval, the implementation process begins, and the budget becomes the financial plan for the local government for the fiscal year. Departments and agencies use the allocated funds to carry out their activities and deliver services to the community. Throughout the fiscal year, local governments monitor their actual revenues and expenses against the budgeted amounts. Regular financial reports are prepared to track performance and identify any variances or potential budgetary issues. In some cases, mid-year budget adjustments may be necessary due to unforeseen circumstances, changes in revenue streams, or emergencies. At the end of the fiscal year, local governments evaluate their budget performance and financial management. This evaluation helps inform future budgeting processes and ensures continuous improvement.

The budgeting process for local governments is typically subject to regulations and legal requirements, and it aims to balance fiscal responsibility with meeting the needs of the community. Public participation and transparency are essential components of the process to ensure accountability and build trust with the residents. In addition to the community, agencies can present budgetary information to stakeholders and donators, showing how funds are allocated and used.

Budgeting is an important part of accounting for every type of entity. However, budgeting for fund accounting differs from general accounting in several key aspects due to the unique characteristics of each accounting method. General accounting focuses on the financial activities of an entire organization, consolidating all financial transactions into a single set of accounts. It aims to provide a comprehensive view of the organization's financial position. Fund accounting, on the other hand, treats each fund as a self-contained accounting entity with its own set of accounts, representing resources with specific purposes or restrictions.

The purpose and usage of funds for general accounting make it suitable for commercial enterprises that aim to maximize profits and shareholder value. Entities that do not aim to make a profit, tend to use fund accounting instead. Fund accounting is commonly used by government entities, nonprofits, and other organizations with multiple funds, where accountability and stewardship of resources are essential. Funds may have specific purposes, such as public safety, education, or social services, that need to be budgeted for. Federal, state, and local governments also need to budget for a reserve fund, where they set aside money for specific purposes, such as emergencies, unexpected expenses, or future projects. These reserves provide a financial safety net and ensure the availability of funds for planned initiatives.

In general accounting, the budgeting process is usually focused on aiming to forecast overall revenues and expenses for the organization as a whole. Budgeting in fund accounting involves creating separate budgets for each fund, detailing the expected revenues and expenses specific to the purpose of each fund. Budgets are prepared independently for each fund and are managed accordingly. Budgetary control in fund accounting is also applied to each fund individually. The focus is on ensuring that the financial activities within each fund adhere to its allocated budget and intended purpose. For general accounting, budgetary control typically involves tracking and managing expenses against the overall budget of the organization.

The budgeting process for each of these accounting types follows strict standards and regulations put in place by third-party organizations. General accounting often follows Generally Accepted Accounting Principles (GAAP) or International Financial Reporting Standards (IFRS) for financial reporting. Fund accounting might follow specific accounting standards tailored to the requirements of government entities or nonprofit organizations, such as Governmental Accounting Standards Board (GASB) guidelines. While both general accounting and fund accounting involve budgeting, the key differences lie in the focus on individual funds, the purpose of the accounting system, and the budgeting and reporting processes tailored to each approach.

In summary, budgeting serves as a cornerstone in fund accounting, providing a framework for financial planning, control, and reporting. It ensures that funds are used responsibly, ethically, and in alignment with the organization's objectives and the expectations of a local government’s community. Budgeting is also crucial in the fifth and sixth principles of fund accounting, financial reporting, and audit requirements. The budget serves as the initial financial plan for the fiscal year. When the actual financial results are reported, they can be compared to the budgeted amounts. This comparison allows for a clear assessment of how well the government adhered to its financial plan and whether any deviations occurred. Budgeting and financial reporting are interconnected processes that work together to enhance their ability to meet audit requirements effectively.

.png?width=70&name=Untitled%20design%20(13).png)

.png)